Over the last 12 months or so, we have witnessed a consistent trend where bad economic news (for example, an increase in unemployment statistics) often results in an increase, rather than a decrease, in broad stock market values. This counterintuitive phenomenon emphasizes how important the outlook for future interest rates is on the value of publicly traded equities. Equity traders would prefer that interest rates begin to fall sooner rather than later, so when news emerges that suggests things aren’t going well, increases in stock prices have often resulted.

During the month of March, three small to mid-size US banks failed. They were the highest profile failures since the 2008 financial crisis. Concerns across the banking sector also spread globally, with UBS purchasing Credit Suisse in an emergency arrangement backed by the Swiss government. So what was the aggregate result of this bad news? Well, global equities continued their upward climb, rising 2.5% for the month and an eye-popping 7.2% for the quarter. Once again, bad news (the bank failures) translated into good news (increases in broad market equity values) as most market players concluded that central banks will be much more reluctant to raise interest rates. The bank failures definitely had a negative impact on the financial sector, but generally helped everything else (at least in the short-term).

Will bad news continue to be good news going forward? Perhaps. And the phenomenon might continue for several quarters if inflation doesn’t continue to decline as anticipated. Over the last few weeks markets have priced in fairly significant declines in future rates … but plausible scenarios certainly remain where interest rates remain stubbornly high and the ‘risk-on’ trades of the last 6 months appear premature. But sooner or later we believe that longer term fundamentals will win out and good news will become the trigger for good news. For now, maintaining broadly diversified exposures which can thrive in a modestly higher interest rate environment continues to be the foundation of our investment thesis.

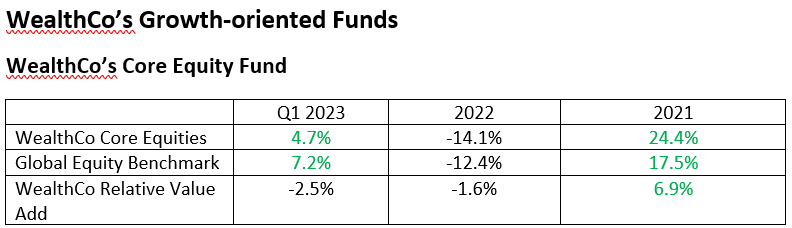

WealthCo’s Core Equity fund posted a return of 4.7% in Q1 2023, underperforming benchmark performance of 7.2%. The fund is up over 9.5% since September 30, 2022 which hopefully indicates that the ‘bottom’ of this most recent public equity cycle is firmly in the rear-view mirror. Positive relative performance during January and February was offset by negative relative performance during March. The fund’s overweight to Small Cap equities was the primary detractor for the quarter. That having been said, our small cap weight has been additive over the last few years and we remain confident that the diversification it offers will continue to add value over the long term. With a 3-year return of 15.1% per annum and a 5-year return of 8.4% per annum, the Core Equity fund has delivered impressive value for long-term investors.

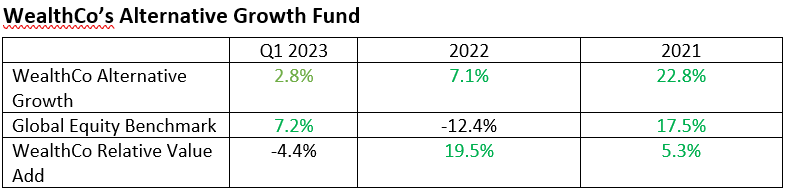

WealthCo’s Alternative Growth fund posted a return of 2.8% in Q1 2023, underperforming benchmark performance of 7.2%. Fund performance was led by strong returns from several of its diversified US Real Estate holdings along its pool of real estate holdings based in Mexico City. Modest write-downs in some of the fund’s private equity holdings offset a portion of the real estate gains. Private market valuations often lag public market shifts and certainly don’t reflect the bounce back in publicly traded equities which we’ve seen over the last six months.

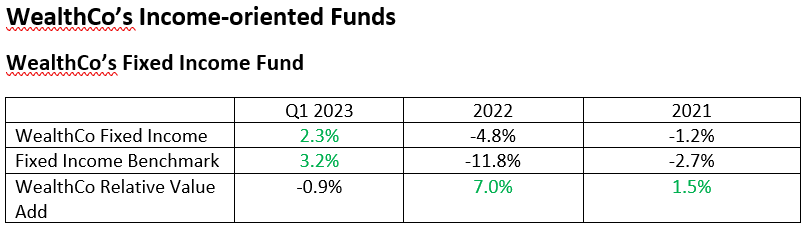

WealthCo’s Fixed Income fund posted a return of 2.3% in Q1 2023, underperforming benchmark performance of 3.2%. The fund’s strong performance was driven by a significant decline in mid to long-term yields in both January and again in March. Fixed income market sentiment oscillated during the quarter, ending with expectations that central banks will proceed with rate cuts sooner rather than later. Mid to long-term yields fell significantly in anticipation of much lower short-term rates in 2024 and beyond. The fund remains conservatively positioned with a relatively short duration compared to most retail fixed income solutions. While this hurt relative performance in Q1 2023, it provides a backstop should interest rate cuts not emerge as quickly as anticipated.

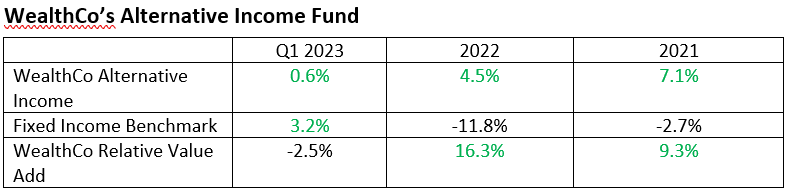

WealthCo’s Alternative Income fund posted a return of 0.6% in Q1 2023, underperforming the fixed income benchmark by 2.5%. The fund’s performance was tempered by its limited exposure to longer duration securities along with its exposure to underperforming publicly traded corporate debt and mortgage funds during the last two weeks of March.

Related Posts