Slow and Steady Wins the Race

We are all familiar with the classic Aesop fable of the ‘Tortoise and the Hare’. It sometimes seems counterintuitive that the slow and steady turtle outperforms the overconfident and aggressive rabbit, but time and time again we are reminded that regular, consistent efforts are the best way to achieve our long-term goals.

2023 Featured a Quick Start, a Frustrating Middle, and a Great Finish!

Looking at investment markets during 2023, the Hare got off to a quick start with public equities rallying quickly in January. But from February through the end of October, both public equity and bond performance disappointed investors as central banks continued to increase short-term interest rates in an effort to quell inflation. Market consensus that we were in a ‘higher for longer’ interest rate environment became very strong with the US 10-Year Treasury bond yielding over 5% on October 23rd and Canadian 10-Year bonds yielding over 4.25%, levels we hadn’t seen in over 16 years.

But the Hare had a great finish ... with both equities and bonds rising significantly in both November and December. Triggered by surprisingly encouraging data points with regard to US inflation and a hawkish tone from the US Fed, both public equities and bonds posted very strong returns to finish the year in anticipation of a series of interest rate cuts beginning in 2024. 10-year yields fell over 1% in less that 2 months ... a startling fast adjustment that the market very rarely sees. Benchmark Canadian bonds soared 7.9% in the last 2 months of year ... its best 2-month performance in over 20 years! Global equities finished strong as well with the benchmark increasing 8.7 over the last 2 months.

So who is ahead now ... the Tortoise or the Hare?

At WealthCo Asset Management, we believe a fully diversified approach to investing is most likely to win out over the long term and to mitigate downside risk along the way. Our target asset allocations continue to recommend a 50% allocation to both private Alternatives (aka the Tortoise) and public (the Hare) markets. Our recommendation is grounded in our belief that there will definitely be time periods during which public markets outperform (as we saw over the last few months of 2023) and there will definitely be periods during which Alternative markets outperform (as we saw through all of 2022 and most of 2021). But forecasting when the inflection points will come, and how long the cycles will last, is incredibly difficult and rarely rewarding.

Therefore we believe that a balance of both approaches smooths out the journey toward our collective investment goals, and will win out over the long term.

Investors assess past performance for a variety of reasons in a variety of ways. And technology has evolved such that it is possible to assess performance over countless time horizons using all sorts of metrics. It is most convenient to assess performance on a calendar year basis ... but rarely (if ever) is a calendar year (or series of calendar years) aligned with a full market cycle or an investor’s actual time horizon.

Over the last 3 months, the Hare (a full allocation to public equities and bonds with no alternatives) is ahead by about 3.5%. Over the last 3 years the Tortoise (a diversified allocation to Alternatives and public markets) is ahead by about 3% per annum (or 9% in total). These results are consistent with the general expectation which we continue to reaffirm with our client investors, specifically:

"Our investment philosophy prioritizes downside protection over upside capture. Put another way, we generally expect to outperform in the short-term when markets are soft or negative, but are likely to lag when markets are hot and running fast. The broad diversification of our portfolios and reliance on bona-fide private market alternatives tempers both short-term gains and losses. We do expect to outperform over the longer term with less volatility than a retail investment structure."

So what can past performance tell us about future performance?

Asset managers (including WealthCo) commonly include a disclosure such as ‘Past performance may not be indicative of future performance’ when communicating investment returns.

Why is this the case? Well, aside from the fact that these disclosures are regulatory requirements (which in itself is an excellent reason), it is important that investors understand that past performance rarely repeats itself, especially in the short term.

Whether we are looking at specific securities, sectors, or broad asset classes, it is much more likely that serial correlation of an assets performance history will be low. Investors who chase recent securities, sectors or asset classes which have recently outperformed are much more likely to be frustrated than those who embrace those which have recently underperformed. And history has also shown us that tactical market timers (like many GIC investors who shunned public markets in Q2/Q3 2023 and embraced 5% GIC rates) usually end up disappointed over the long term.

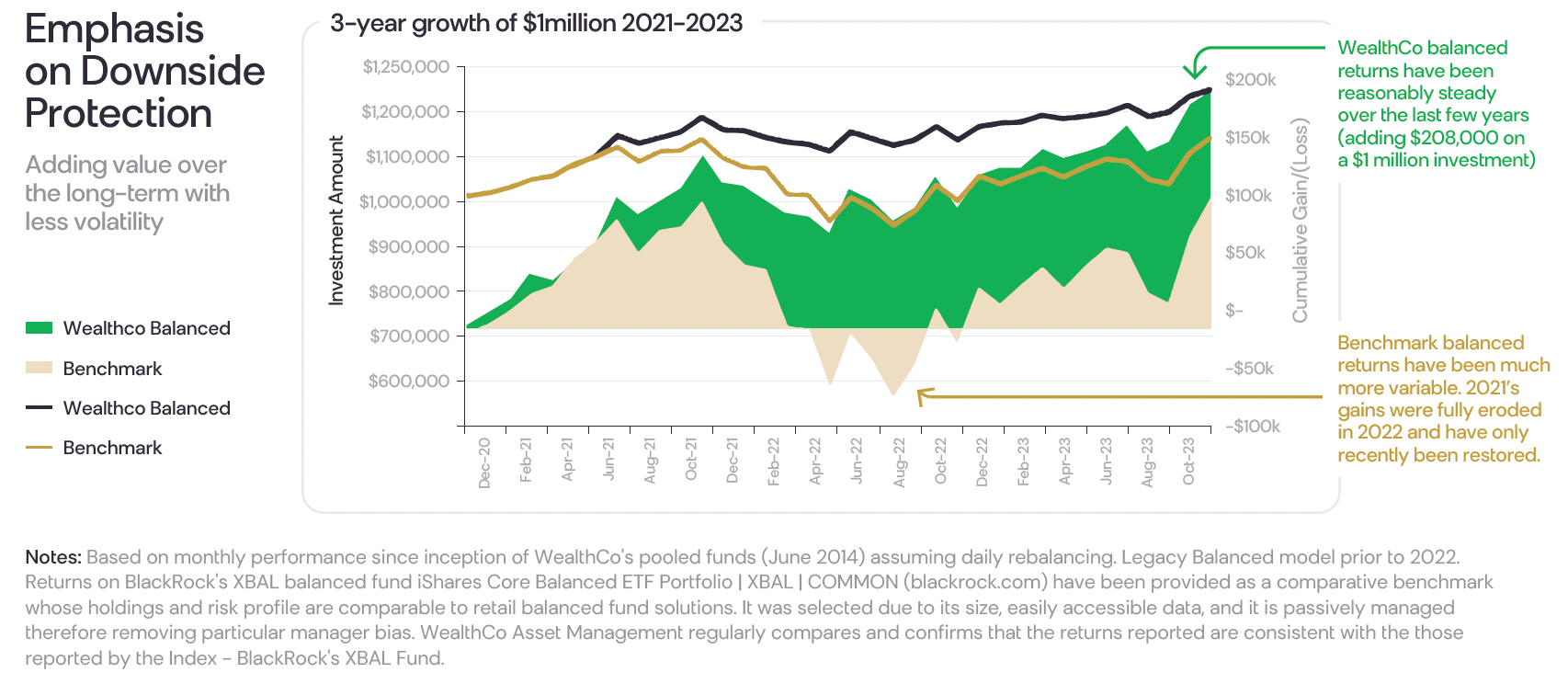

However, while we would reaffirm that in no way can WealthCo- (or any other investment manager for that matter) guarantee anything with regard to future performance, we do believe that past performance trends over the mid to long term, particularly with regard to risk metrics for diversified portfolios, can be predictive of future trends. The standard deviation, or volatility, of WealthCo’s Balanced Target Allocation is roughly half that of that of BlackRock’s XBAL ETF (which is representative of typical retail balanced funds focused on equities and bonds).

The resulting drawdowns of a WealthCo balanced allocation have been much less significant, and we reasonably expect the volatility of our target allocations to be lower going forward:

So what lies ahead?

For balanced WealthCo investors, returns for calendar year 2023 (after investment management fees but before advisory fees) were strong (approximately 9.1%). Growth oriented portfolios performed slightly better. Annualized balanced performance over the last 3 years was 6.6% while it was 6.4% over the last 5 years ... indicative of the ‘slow and steady’ nature of our investment model. Given the multiple shocks to the global economy over the last few years, we are very pleased with these results.

2023 closed with general market consensus that interest rates have peaked and that central banks will cut rates multiple times in 2024. If that scenario plays out, we anticipate particularly strong returns from our both our Alternative pools as well as our Fixed Income pool. Returns from our equity pool should be solid, but we should keep in mind that the market has priced in much of the ‘good news’ embedded in the new view on interest rates. It will take a few months, if not quarters, for our Alternative pools to fully price in the new perspective.

We also expect the $US Dollar to strengthen somewhat versus $CAD in 2024 which will help returns. The $US Dollar fell significantly during the last two months of 2023 in anticipation of future Fed rate cuts and- created significant headwinds for both Alternative pools. But from our perspective, we expect the Canadian central bank to cut rates sooner than the US which should limit any further appreciation of $CAD.

But we are also cognizant that forecasting short-term interest rate movements is extremely difficult, and that the ‘general consensus’ seems to have been wrong more than right over the last little while. Collectively we may well have to be patient to see short-term rate cuts, but that’s a scenario that we believe we are well positioned for in both our public market and Alternative pools.

As for the battle between the Tortoise and the Hare, it’s important to keep in mind that when it comes to personal investing, rarely is there a ‘Finish Line’ and that investment horizons continue to extend into the future. With this in mind, we remain confident that our ‘slow and steady’ approach and commitment to bona fide Alternatives, will provide our investors with the long-term results they are looking for with comfort and confidence that their short-term risks are limited.

As always, our sincere gratitude for your confidence and support of our investment model.

Wishing all of you the very best in 2024!

Related Posts