Financial Planning

General Interest - Personal

Investment Planning

The Great Wealth Transfer is Coming: Is Your Family Ready?

November 08, 2021

What is ‘The Great Wealth Transfer’? That wealth transfer refers to the accumulated estate wealth that will be changing hands from parents and grandparents to their beneficiaries in the coming decades. It is forecasted that in Canada $1 trillion will be bestowed by 2026. That’s a lot of money. That’s almost enough to orbit to the International Space Station on the SpaceX rocket 20,000 times (at the current price tag of $55 million per trip), if that particular voyage is something that tickles your fancy.

While multi-generational estate planning has existed in some way, shape or form for as long as assets have existed, this will be the largest redistribution of wealth in human history. Which raises some questions.

How can Benefactors Best Prepare for This Wealth Transfer?

Research firm Strategic Insights reports that 32% of wealthy Canadians are concerned about how their children will handle their inheritance, and 36% don’t feel that their heirs have the financial acumen to properly manage it.

“A lot of money is going to be placed in the hands of a generation that, in general, is undereducated when it comes to traditional investing and financial planning,” WealthCo Financial Advisor Craig MacFarlane points out. “This could lead to even more money flowing through investment brokerage apps and reckless trading on these platforms in general.”

It is never too early to draw up a wealth transfer plan. These plans can always be updated and amended as circumstances change but having something in place is critical. These aren’t fun discussions to have, but they are necessary. Conversations about wealth transfer with family members can actually strengthen relationships across generations, and it provides opportunity for some financial education. Factors in legacy planning may include the following:

- Family dynamics – any ambiguity in the planning could result in tensions

- Any conditions that may be required with the bequest (heirs receiving their funds at a certain age or upon completion of post-secondary education being two such examples of conditions)

- Whether funds will be distributed as a lump sum or through multiple payments

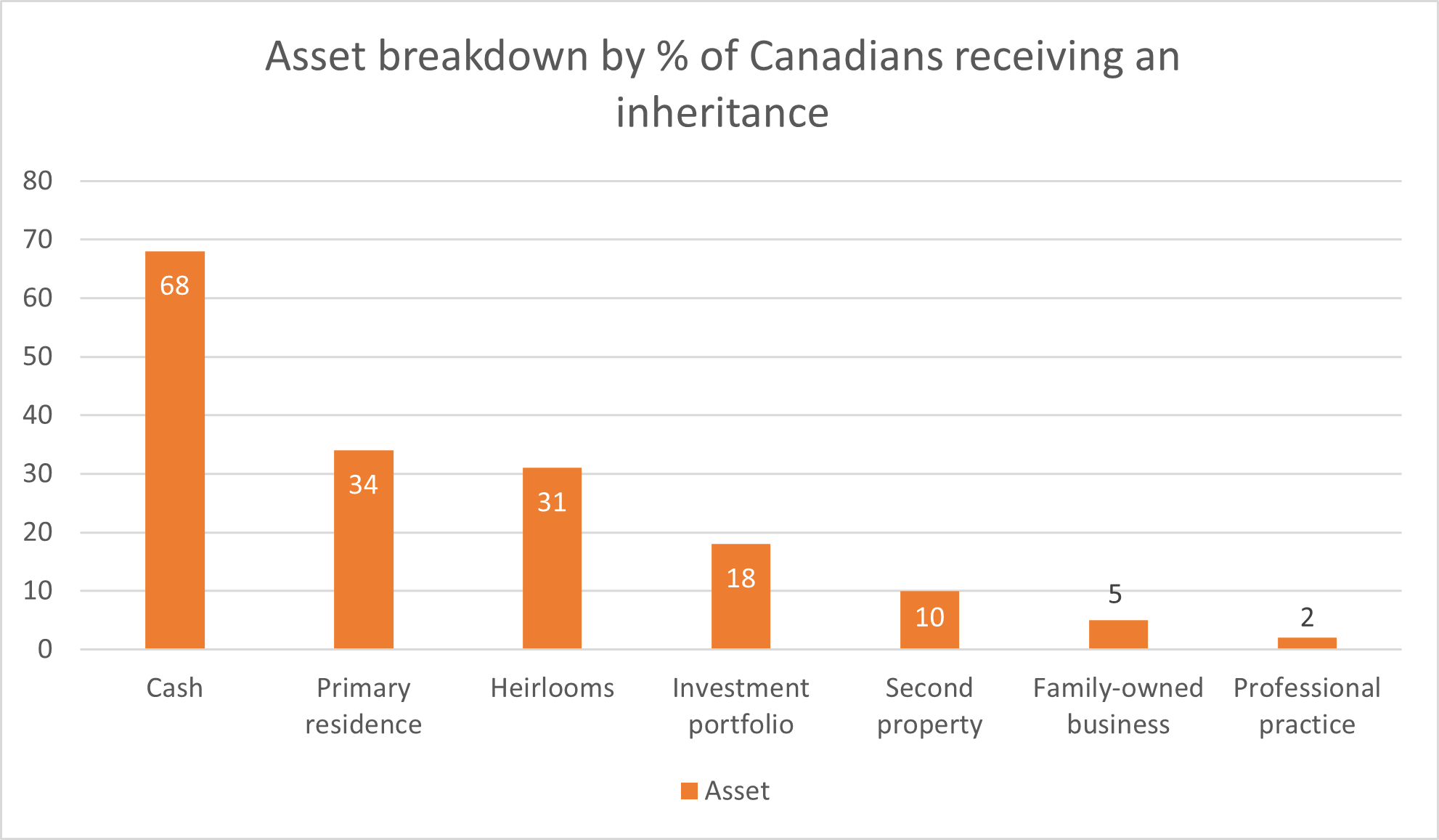

- Specific assets or heirlooms that should be left to particular individuals

- Charitable giving intentions

- Taxation considerations

Benefactors have worked hard in building their wealth, and it’s important to ensure proper and thoughtful preparation to honour their wishes in how said wealth is ultimately distributed. This approach may even involve ‘giving while living’.

“Typically, the majority of wealth transfer takes place at death, through registered beneficiaries or a will,” MacFarlane shares. “However, it is becoming increasingly common to see gifting taking place during the clients’ life, so they can see the enjoyment of their legacy passed on while they are still alive.”

How can Beneficiaries Best Prepare for Wealth Transfer?

We’ve all heard the tragic stories of lottery winners who go broke (studies put the number at 70% of lottery winners that end up filing for bankruptcy). No wonder a third of wealthy Canadians have concerns about their heirs. So, how can beneficiaries best prepare for their financial journey ahead?

“With an influx of wealth, the value of a financial planner and a clear financial road map will rise as well,” MacFarlane predicts. “Most average investors will typically be overwhelmed when a windfall arrives, and sound advice becomes paramount.”

Step one in mitigating the risk of a squandered inheritance comes back to having those intergenerational conversations. Presumably, by having built a level of wealth, the benefactor has at least a modicum of financial literacy, so use this as an opportunity to educate the next generation.

“The best advice is to educate yourself and be open with your children about the future,” MacFarlane recommends. “Money can be a taboo subject but the more engaged and educated everyone is, the easier the transition will be. Have your children or beneficiaries in general involved in future financial planning meetings. Introduce them to your advisory team (CPA, financial planner, etc.) Make sure everyone is on the same page.”

And as for the beneficiaries themselves, taking the time to get educated on financial literacy is key. Just consider how differently things may have turned out for that 70% of bankrupt lottery winners if financial education had been a condition of their winnings. This is where a trusted advisor can be a gamechanger. They will work with beneficiaries to create a financial plan that will protect and grow their wealth while still allowing them to enjoy it.

What Role do Financial Planners Play in This Wealth Transfer?

Once an inheritance is received, the reality is that the beneficiary may have a different opinion then their benefactor did as to how their portfolio should be managed. It’s no longer safe to assume that any family money will stay put. Especially given the availability of investment tools and apps that have entered the marketplace. Even if a firm has protected and grown the family wealth for years, the risk does exist that a beneficiary may choose an alternate financial planning path going forward.

Yet again, it all comes back to education. Financial planners and wealth management firms have a huge role to play in demonstrating their value as compared to the alternatives.

WealthCo’s integrated advisory model uniquely positions us and our accounting firm partners to best support our clients through the entire wealth planning and management process.

“Competition will continue to rise,” MacFarlane notes, “but firms offering the best, most personalized solutions, with proper advice, will flourish.”

Note: this article is part of our four-part series on Millennial Investment Trends. Check out the other articles in the series:

Growth of the Sustainable Investing Movement

Related Posts